Highlights:

- In April, both retail and institutional investors showed reduced interest in cryptocurrencies, as reflected in the falling open interest figures. Exchange open interest for BTC and ETH decreased by more than -19%. When examining the CME, which caters more to institutional participants, the decrease was even more pronounced: open interest for BTC fell by -24.74% and by -41.8% for ETH.

- On April 3, Bitfinex introduced volatility perpetual futures for Bitcoin and Ether. The futures are linked to the Volmex Implied Volatility indexes, specifically the Bitcoin Implied Volatility Index (BVIV) and Ethereum Implied Volatility Index (EVIV), which monitor the 30-day expected volatility of BTC and ETH options contracts.

- For the first time in over six months, the Open Interest (OI)-weighted funding rate for BTC and ETH turned negative. BTC experienced this on April 14, 15, and 18-23, while ETH saw similar trends on April 14, 17, 20, 22, and 23.

Forecast

Between May and October, both traditional finance and the crypto markets typically experience a period of stagnation, often referred to as the “Sell in May and go away“ phenomenon. Historical data from Coinglass shows that during these months, derivatives open interest and perpetual funding rates remain stagnant. This stability coincides with a lack of volatility and performance for both BTC and ETH. They historically averaged gains of 6.49% and 4.01% in Q3. If historical trends continue, derivatives will see reduced activity in the next few months.

Sentiment

Retail and institutional investors are cautious, as decreased open interest indicates they await clearer market direction. This reduction in activity has lowered liquidity and with declines in futures premiums and funding rates, the market has shifted from March’s euphoria to caution.

Analysis

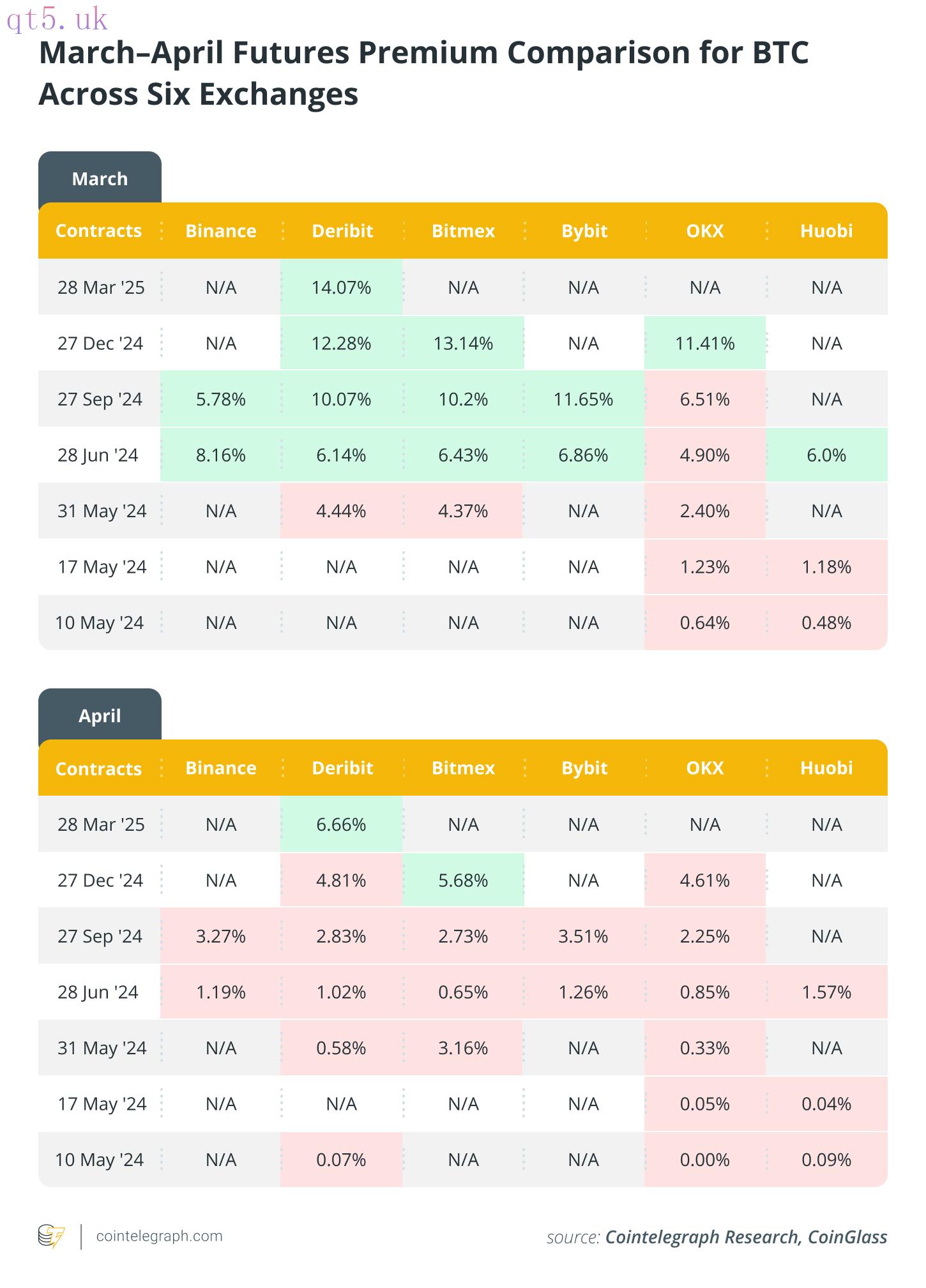

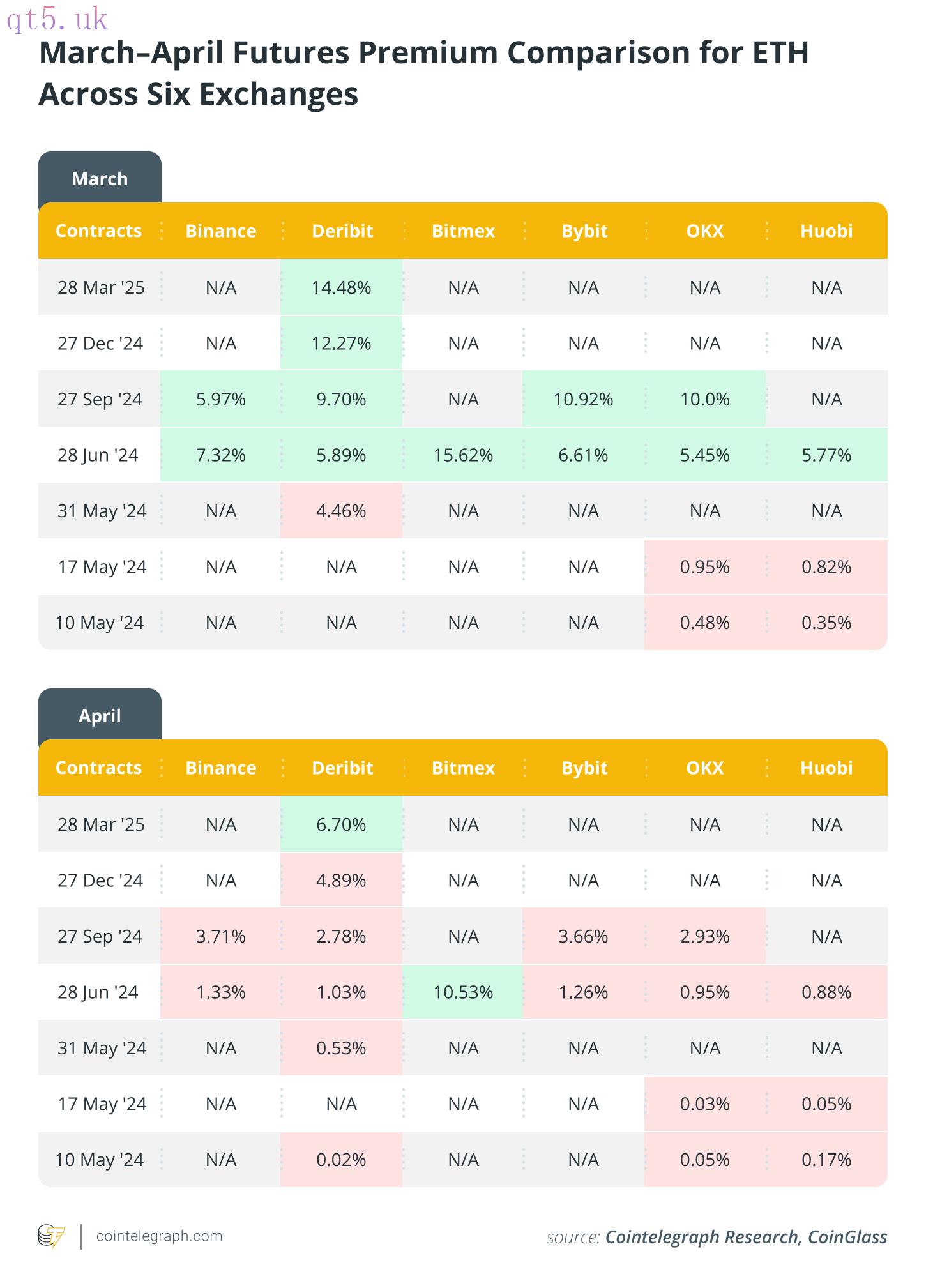

In April, derivatives held a 60% market share in crypto trading volume, a drop from February’s 70.1% and March’s 67.8%. This change points to a decreased interest in derivatives trading. Additionally, two other pieces of data are evidence for this trend. First, the futures premium has declined. Across major exchanges such as Binance, Deribit, BitMEX, Bybit, OKX, and Huobi, the basis rate for both BTC and ETH contracts fell below 5% by the end of April, irrespective of the expiry date. Investing in U.S. Treasury bonds has become more lucrative while involving significantly less risk than a cash-and-carry strategy on cryptocurrencies.

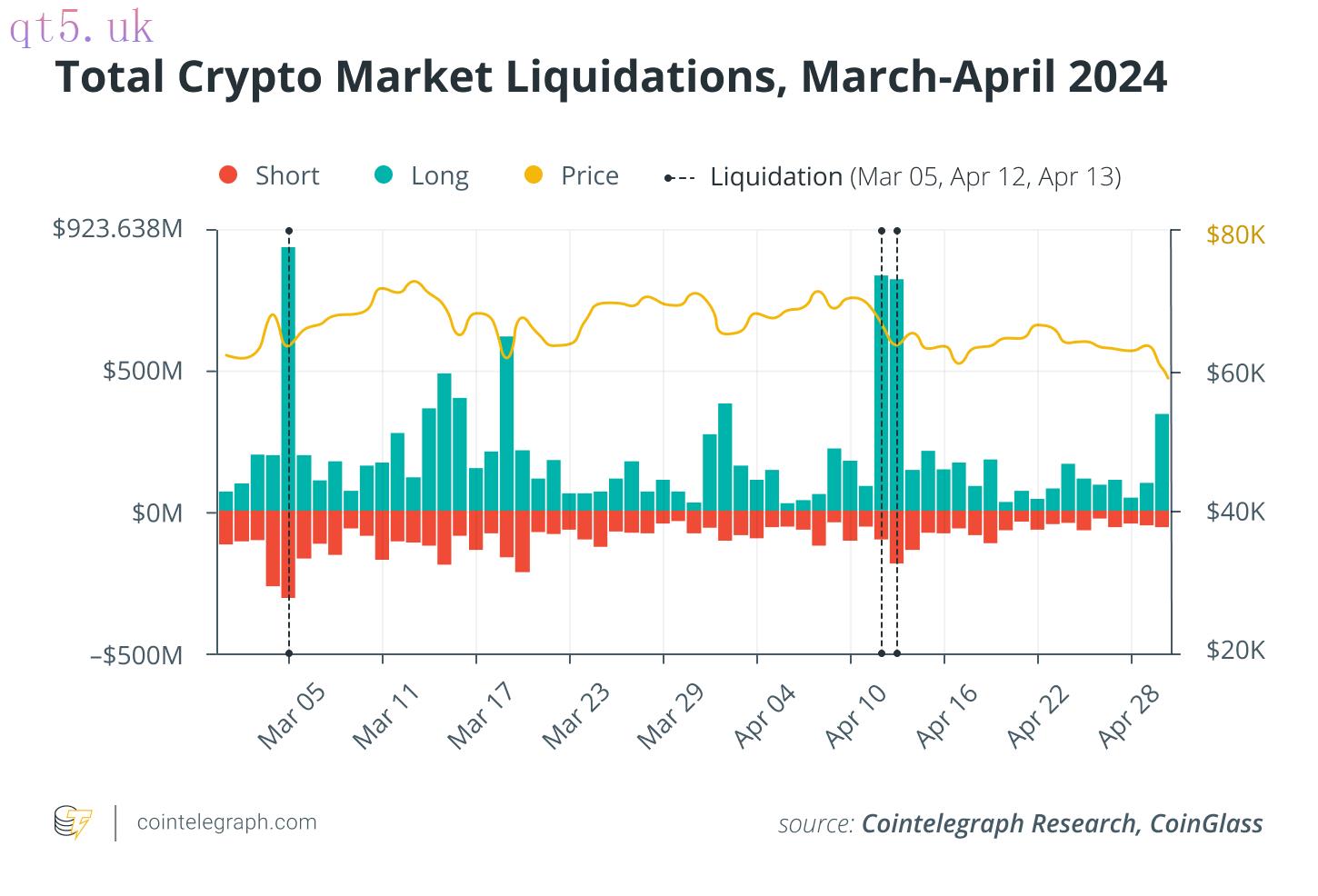

On April 12 and 13, long liquidations on Bitcoin totaled $784.714 million and $771.441 million, respectively, triggered by escalating geopolitical tensions between Iran and Israel. Historically, long liquidations exceeding $700 million in the cryptocurrency market are uncommon. Since 2023, such events have occurred only twice: on Aug. 17, 2023, when SpaceX sold a large amount of Bitcoin, and on March 5, 2024, when $879.655 million was liquidated following outages at major cryptocurrency exchanges Binance and Coinbase.

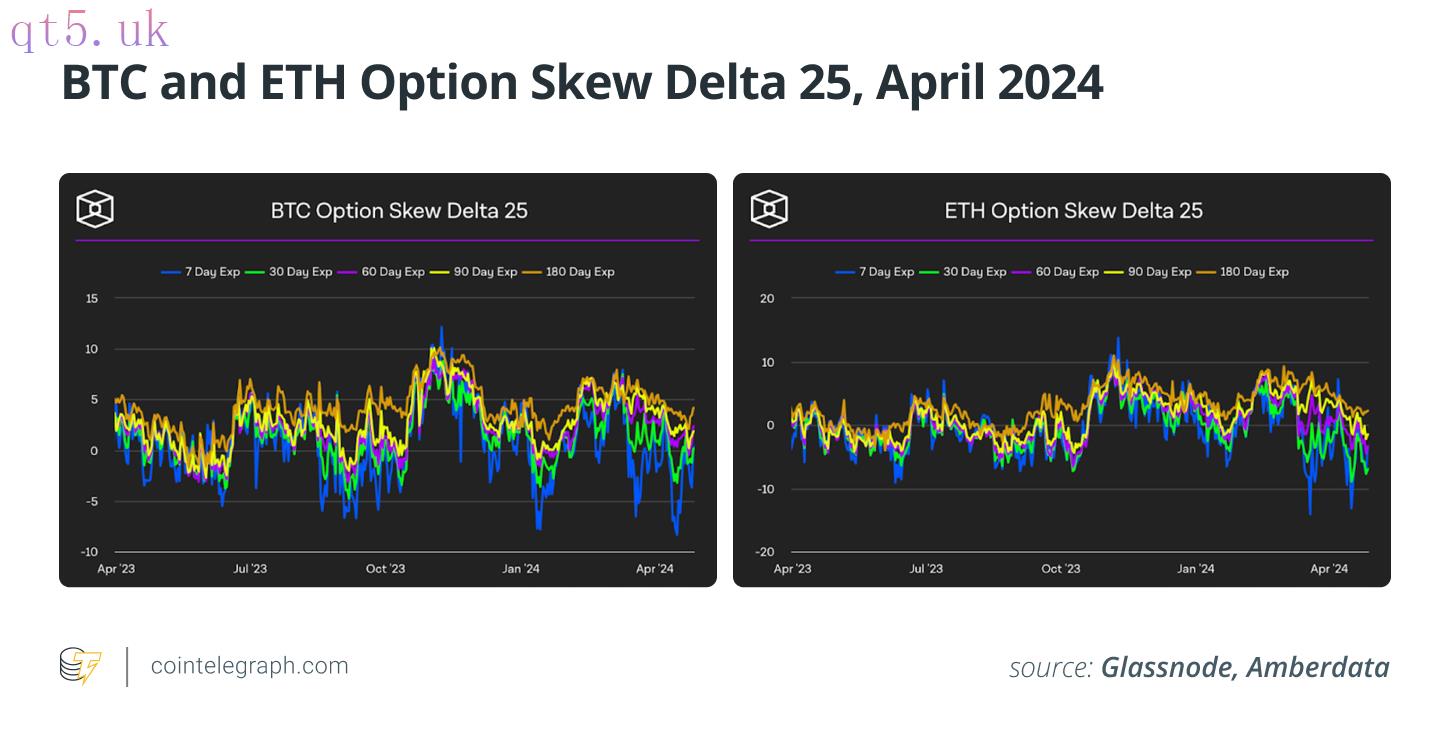

Such large-scale liquidations demonstrate the market’s sensitivity to sudden changes, which is also evident in derivative metrics such as the option skew delta 25. BTC’s 60, 90, and 180-day skews remained positive. However, its 30-day and 7-day skews turned negative and stayed there until the end of April. ETH displayed a different pattern, showing negative skews across the 7, 30, 60, and 90-day periods, signaling a cautious investor outlook due to fear of price declines in the short to medium term.

Only ETH’s 180-day skew remained positive. The negative outlook may be rooted in Solana surpassing ETH in decentralized exchange volume and establishing itself as a significant competitor.

download

download download

download website

website