Highlights

- Bitfinex Securities El Salvador issued tokenized debt to fund the construction of a new Hampton by Hilton at El Salvador International Airport. The project aims to raise $6.25 million with a 10% coupon over five years. A HILSV token will be issued on the Liquid Network and traded against U.S. dollars and USDT.

- Grand Base, a tokenization protocol on Coinbase’s layer-2 Base blockchain, experienced a $1.7 million loss from a private key compromise. The incident caused the protocol’s native token GB to plummet by 99% within 24 hours.

- Circle, the issuer of USDC, deployed a new smart contract. The contract enables investors to instantly swap BlackRock’s BUIDL, a tokenized fund that offers U.S. dollar yields, for USDC to maintain a 1:1 peg.

Forecast

Over the next quarter, we expect to see a continued rise in the adoption and development of tokenization projects. The integration of BlackRock's BUIDL token with USDC will likely attract further institutional investment into tokenized assets. This will likely increase the market cap of tokenized U.S. Treasury products, which currently stands at $1.18 billion. Additionally, lending protocols that target emerging markets are expected to adopt stricter risk management practices due to recent defaults.

Sentiment

Despite the recent security breach in Coinbase’s asset tokenization protocol and defaults on undercollateralized loans on Goldfinch, a DeFi tokenized credit platform, heavyweight financial institutions such as BlackRock, Deloitte, and Moody’s continue to express interest in the asset tokenization sector. Additionally, the engagement of certain central banks projects confidence in the potential of RWA.

Analysis

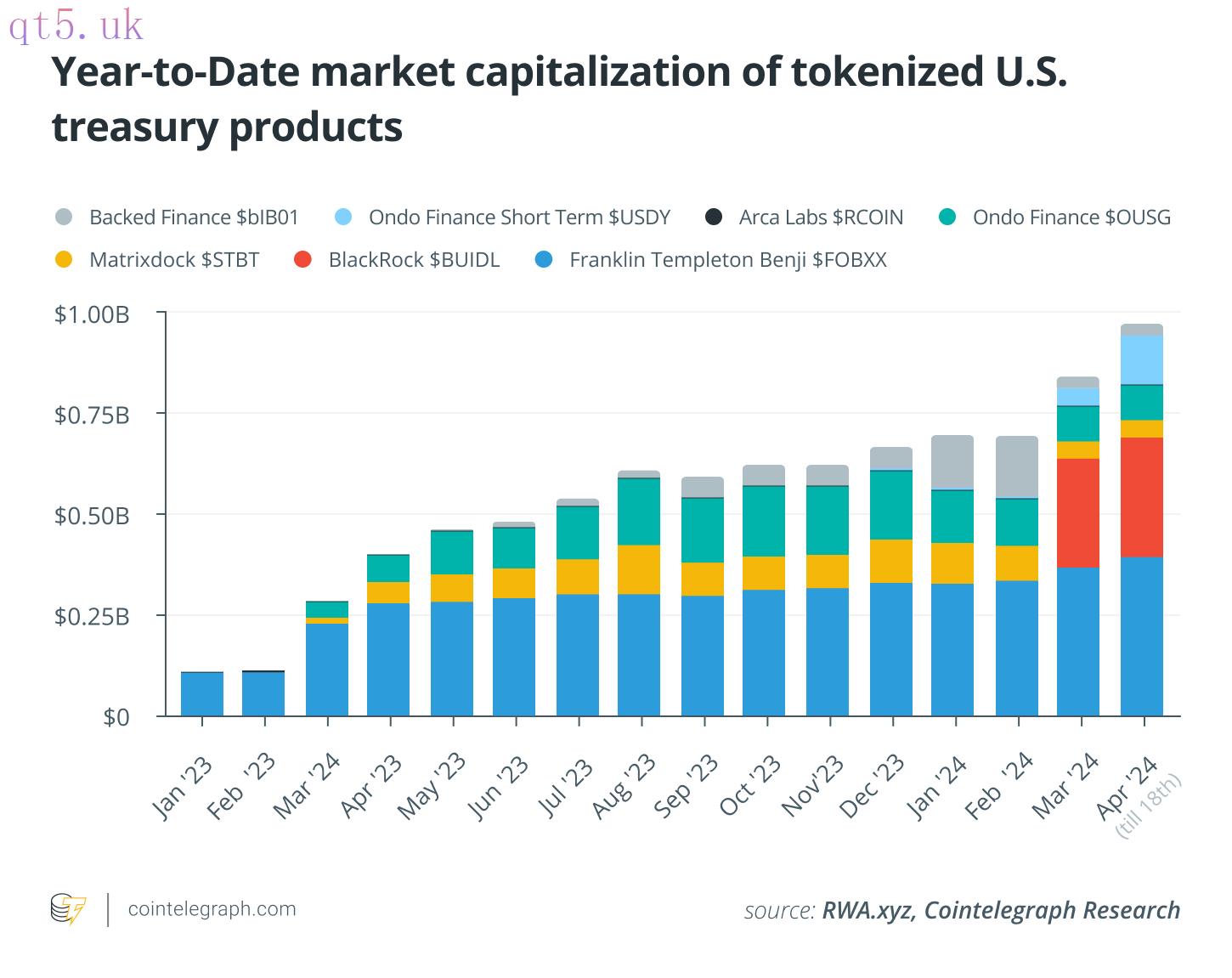

Tokenized U.S. Treasury products have remained stagnant, with market capitalization oscillating between $550 million and $700 million since mid-2023. However, following the introduction of BlackRock’s tokenized fund BUIDL on March 20, these products saw an increase in value and reached $1.18 billion by April 18. The growth primarily resulted from the AUM gains of four products: BlackRock's BUIDL (+$297.36 million), Franklin Templeton Benji Investments' $FOBXX (+$39.19 million), Ondo Finance’s USDY (+$85.4 million), and Superstate’s $USTB (+$66.5 million). Together with Ondo Finance’s OUSG, these products represent 84.37% of the industry.

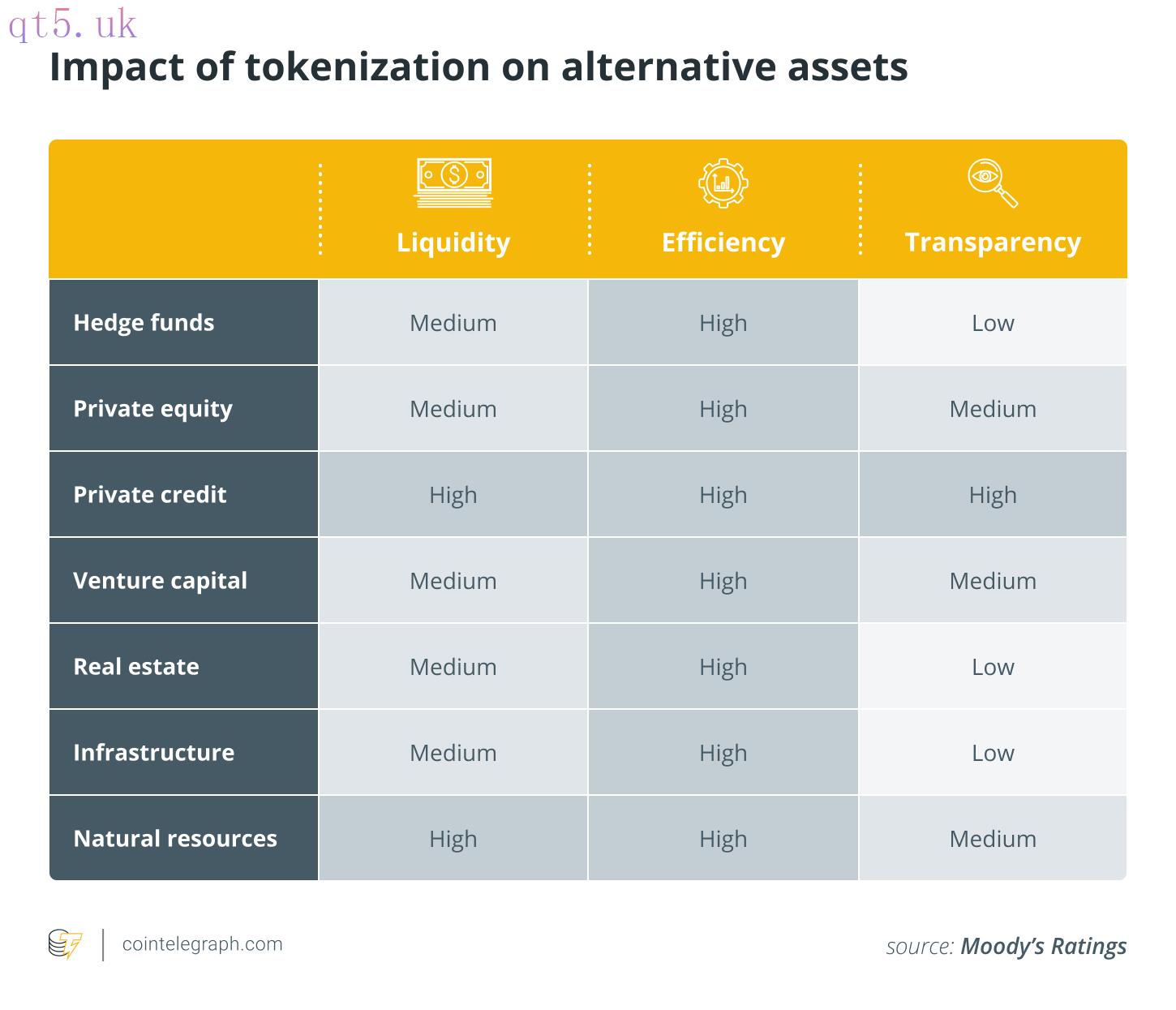

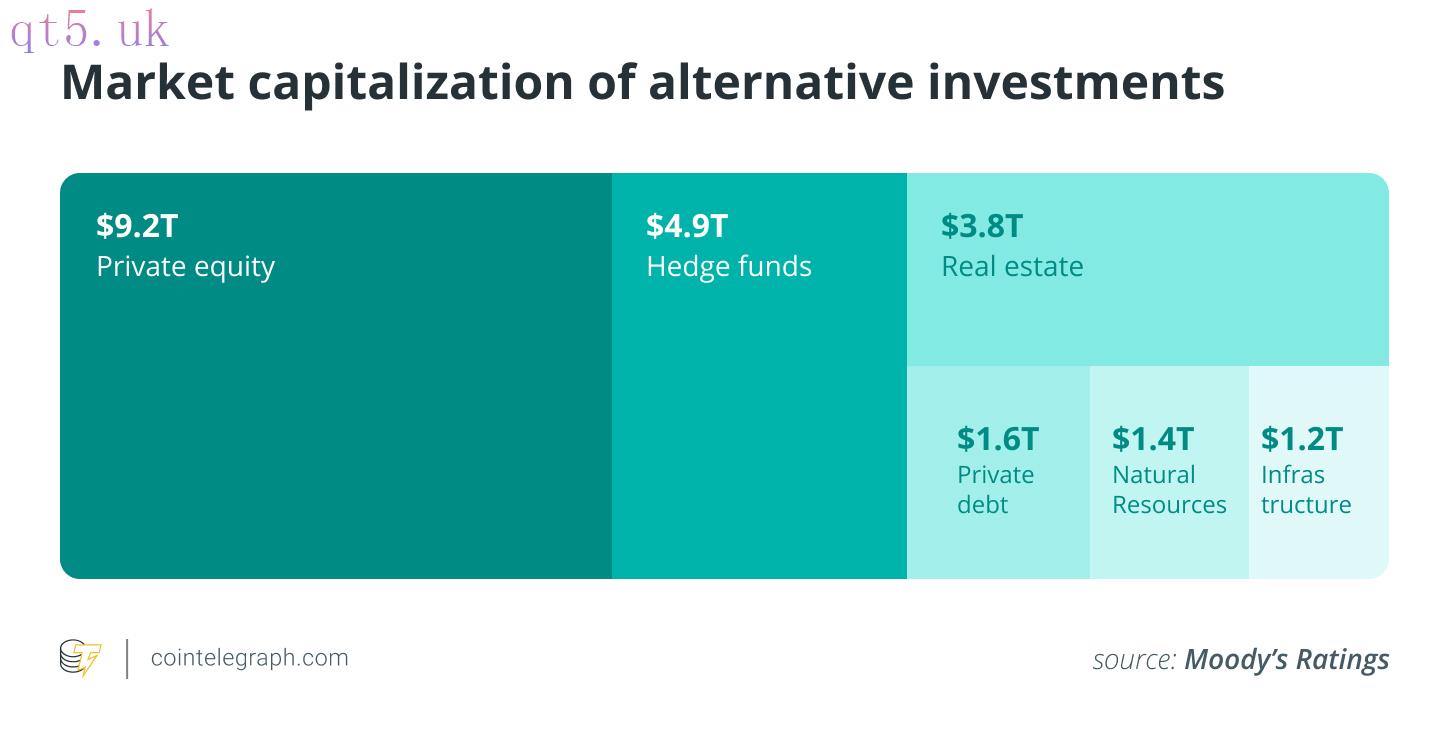

BlackRock is not alone in recognizing the potential of asset tokenization; it is joined by major financial institutions and regulators globally. On April 17, Moody’s highlighted that tokenization will significantly impact the $22 trillion alternative assets market by enhancing liquidity and accessibility. Similarly, in the same month, Deloitte forecasted that tokenization could generate trillions in new value for the financial sector this decade. These analyses converge on the idea that tokenization can address the liquidity challenges in alternative investments, such as private equity and real estate, which often involve long lockup periods restricting capital access.

Despite the potential of tokenization, recent incidents in the crypto lending sector reveal significant risks, especially with undercollateralized lending. Goldfinch has now experienced its third default, with Lend East failing to repay a substantial portion of a $10.2 million loan. This event follows two previous defaults: a $5 million loss with Kenyan company Tugende and a $7 million loss from US-based credit fund Stratos. Collectively, these defaults amount to nearly $17.9 million and represent 23.84% of all active loans on Goldfinch as of April 19. These defaults showcase fundamental issues in the protocol’s approach to assessing and underwriting loans, particularly in emerging markets where high yields often come with high risks. The repeated losses also highlight a persistent underestimation of these risks and a lack of robust risk management processes.

download

download download

download website

website