Highlights:

- Bitcoin (BTC) closed out April down nearly 16% and thus saw its worst month since November 2022. This ended a seven-month rally mostly driven by the anticipation and launch of U.S. spot Bitcoin ETFs.

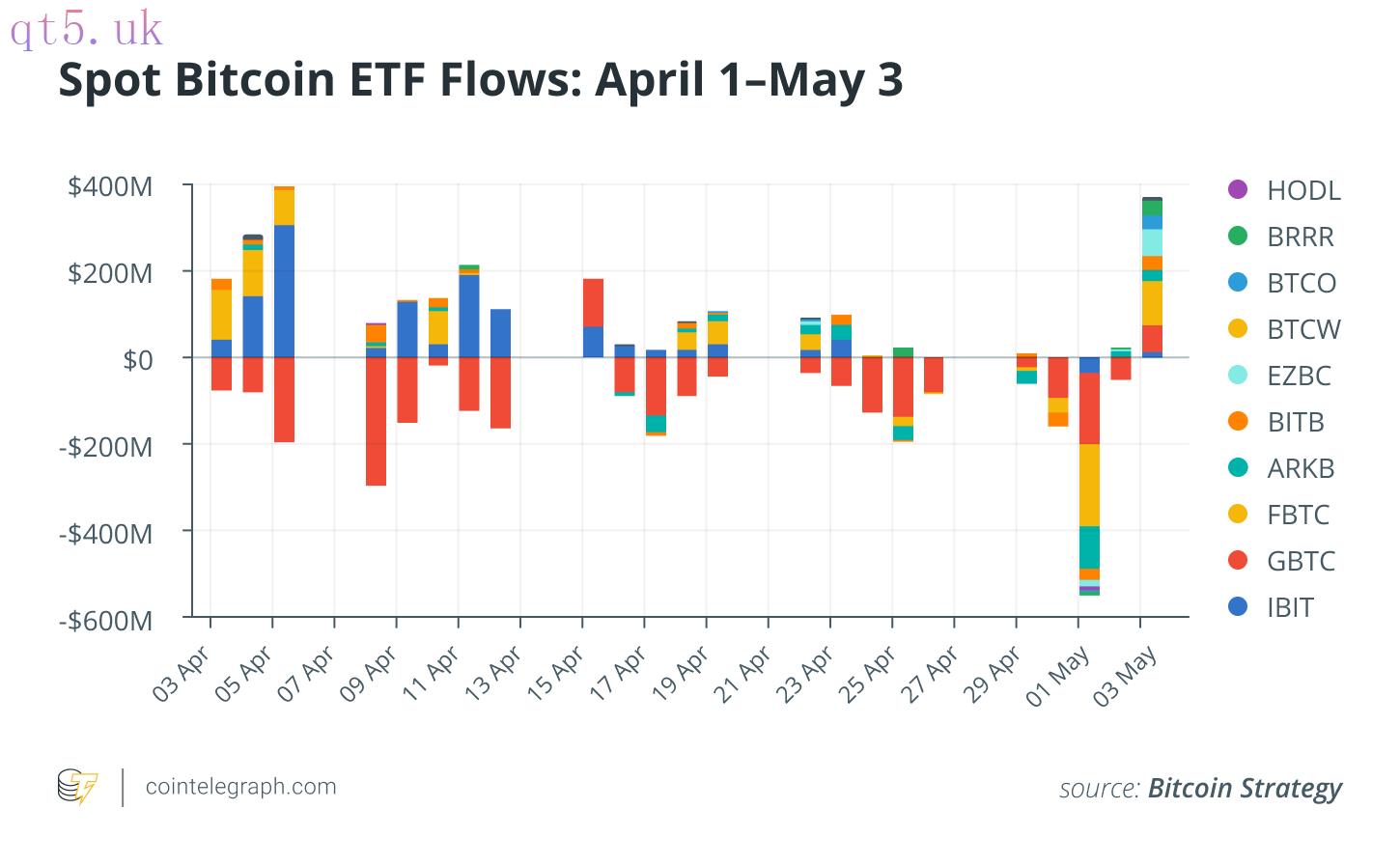

- U.S. spot Bitcoin ETFs saw $343.5 million in net outflows. April was thus a cooling-off period for these investment products after the strong $4.6 billion influx of March. This was the first month of outflows from the new ETFs since their launch in January.

- Hong Kong’s first Bitcoin and Ether ETFs debuted with $12 million in combined trading volume and $292 million worth of net inflows. Analysts predict that the HK ETF might attract $1 billion over two years, foreseeing participation from wealthy Chinese investors in Hong Kong.

Forecast

The key determinants of Bitcoin’s trajectory in the coming month will remain ETF inflows. Bitcoin’s supply will remain highly illiquid and may experience increased volatility due to accumulation by long-term investors. Expectations of an interest rate cut in Q3 2024, which would enhance liquidity in the financial markets, have been lowered.

Sentiment

Bitcoin’s price increase at the start of the year was primarily fueled by ETF inflows, which have now moderated. With reduced expectations for interest rate cuts, market sentiment has shifted toward caution, if not negativity.

Analysis

Bitcoin closed April with a nearly 16% decline, marking its worst performance since November 2022. The 16% decline in BTC’s price was influenced by a substantial $343.5 million net outflow from U.S. spot Bitcoin ETFs in April. The large monthly outflows came predominantly from GBTC with $2.5 billion and ARKB with $86.3 million. On May 1, IBIT had its first-ever day of outflows, and FBTC led outflows with $191 million. Previously, inflows from these two funds had offset the large outflows from GBTC. The recent outflows can be linked to the broader macroeconomic factors last month. They included ongoing high inflation and strong nominal growth in the U.S. economy, which has tempered expectations for Federal Reserve rate cuts. With the increased tensions in the Middle East, most risk assets, including Bitcoin, have recorded negative returns.

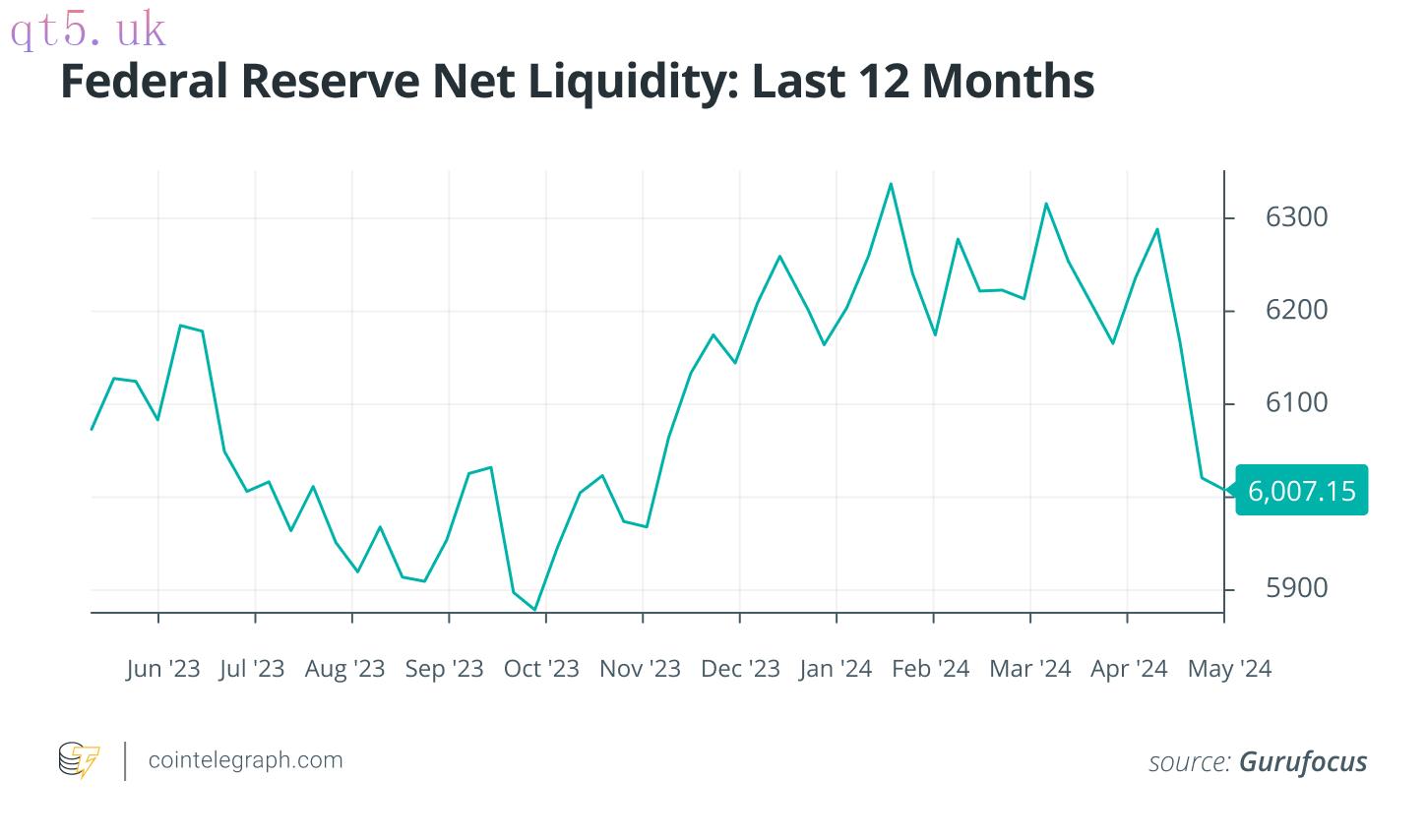

Bitcoin’s market dynamics have been closely tied to the Federal Reserve’s liquidity management. As of the end of April 2024, the Fed’s net liquidity hit its lowest point of the year. This decline can be attributed to the continuation and impact of the quantitative tightening (QT) program. The latter involves reducing the Fed’s balance sheet size, primarily by letting bonds mature and by selling securities. This monetary policy hinders the creation of liquidity that could support BTC’s price. However, the Federal Reserve’s decision to slow its QT program, coupled with the U.S. Treasury’s initiation of a buyback on less liquid securities is projected to prop up financial markets shortly.

The launch of Hong Kong’s first spot Bitcoin and Ether ETFs in April started with $292 million worth of net inflows, slightly below the $300 million target anticipated by ETF analysts. The Hong Kong ETF alone may not be large enough to significantly impact the broader market. Inflows could also be limited due to stringent regulatory differences with mainland China, where cryptocurrency activities are heavily restricted. Furthermore, the new ETFs are excluded from a program that allows Chinese investors access to Hong Kong ETFs if they have no Hong Kong passport.

download

download download

download website

website